1Methodology and data sources

This report makes specific claims: market revenue figures, shortage-list day counts, price bands, state-access tallies, adverse-event frequencies, and AI-citation rates. Each number comes from a named source and a dated snapshot. Four rules govern every chapter.

- Every number traces to a source. Each cited statistic resolves to a public document, a public database, a published clinical trial, or a documented internal dataset. Where a figure is derived rather than reported, the derivation is shown. Where a figure is an industry estimate rather than an audited number, it is labeled an estimate.

- Data is frozen and dated. Sources that change over time (provider pricing, FDA shortage status, AI-citation behavior, keyword volume) are captured as dated snapshots, with a freshness date next to volatile numbers.

- Confidence is disclosed. Most chapters separate high-confidence reported facts from medium-confidence estimates and lower-confidence inferences, and list what was not measured.

- Compounded medications are not FDA-approved as final products. Wherever the report draws on compounded-market data, it states this. Compounded preparations are made by state-licensed pharmacies under physician prescription and are not reviewed by the FDA for safety, efficacy, or quality as finished products.

The report draws on seven categories of source: the FDA Drug Shortage Database, the FDA Adverse Event Reporting System (FAERS), Novo Nordisk and Eli Lilly public financial disclosures, published clinical trials (STEP, SURMOUNT, SELECT, SUSTAIN), SEMrush keyword data, public telehealth pricing pages and public regulatory directories (NABP and LegitScript), and one original dataset: a weekly 25-query AI-citation panel documented in Chapter 9.

Editorial independence

Majesta Health publishes this report, which raises an obvious question: is the analysis tilted toward the publisher? The report is built to answer no in ways a reader can check. Majesta is treated as one data point, not the conclusion. In the pricing scorecard it is one row among competitors, described in the same neutral terms. In the AI-visibility chapter, the report discloses that Majesta was cited on 0 of 25 queries, the least flattering possible finding for the publisher, and prints it rather than hiding it. If a reader removed every mention of Majesta, the findings would stand unchanged. That is the test the report holds itself to.

2Market size and growth, 2022 to 2026

In 2025 the global GLP-1 receptor agonist market crossed $70 billion in annual revenue for the first time. Novo Nordisk and Eli Lilly together collected $71.1 billion from their GLP-1 franchises in 2025 alone:

- Novo Nordisk semaglutide franchise (Ozempic, Rybelsus, Wegovy): $34.6 billion, up 14 percent year over year.

- Eli Lilly tirzepatide franchise (Mounjaro, Zepbound): $36.5 billion, up roughly 100 percent year over year, making tirzepatide the world's best-selling drug in 2025, ahead of semaglutide and ahead of Merck's Keytruda.

For a category worth roughly $7 billion combined in 2020, the trajectory is rare. It roughly doubled every 24 months between 2020 and 2025.

| Year | Novo semaglutide franchise | Lilly tirzepatide franchise | Combined |

|---|---|---|---|

| 2020 | ~$7 billion | Not yet launched | ~$7 billion |

| 2022 | ~$11.5 billion | ~$0.5 billion | ~$12 billion |

| 2023 | ~$21 billion | ~$5.2 billion | ~$26 billion |

| 2024 | ~$30 billion | ~$18 billion | ~$48 billion |

| 2025 | $34.6 billion | $36.5 billion | $71.1 billion |

The product mix shift, diabetes to obesity

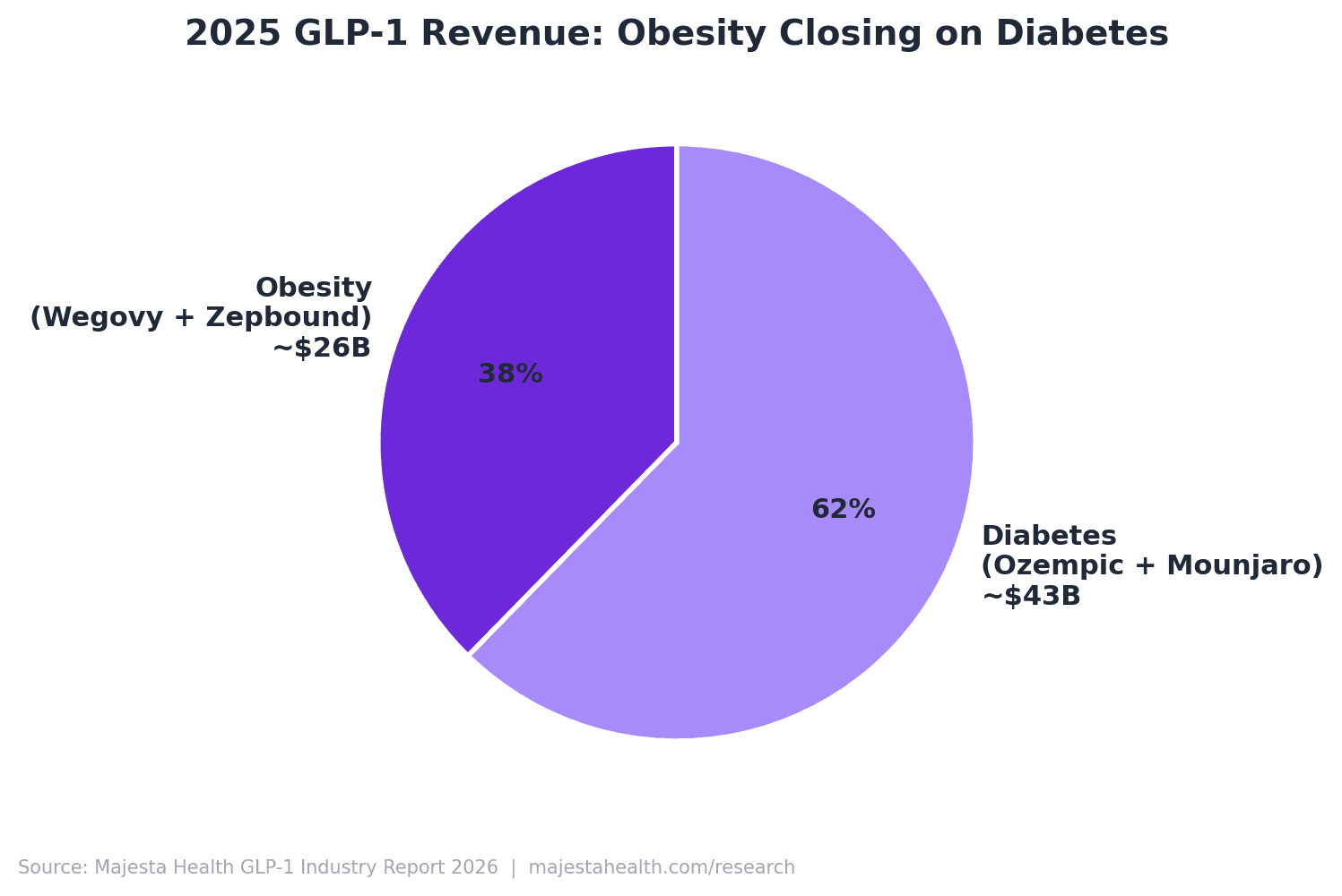

Within both franchises, the obesity indication overtook diabetes as the engine of growth. Wegovy reached $12.5 billion in 2025 (up roughly 134 percent) while Ozempic reached $20.1 billion (up roughly 6 percent). Zepbound reached $13.5 billion (up 175 percent) while Mounjaro reached $23.0 billion (up 99 percent). In 2025 the obesity indication accounted for roughly $26 billion in combined Wegovy and Zepbound revenue against roughly $43 billion for the diabetes indications, and obesity is forecast to overtake diabetes in absolute GLP-1 revenue during 2026.

Applying a midpoint US revenue share of roughly 70 percent to the 2025 combined $71.1 billion gives a US 2025 GLP-1 brand-name revenue of roughly $49.8 billion, before any compounded market is counted.

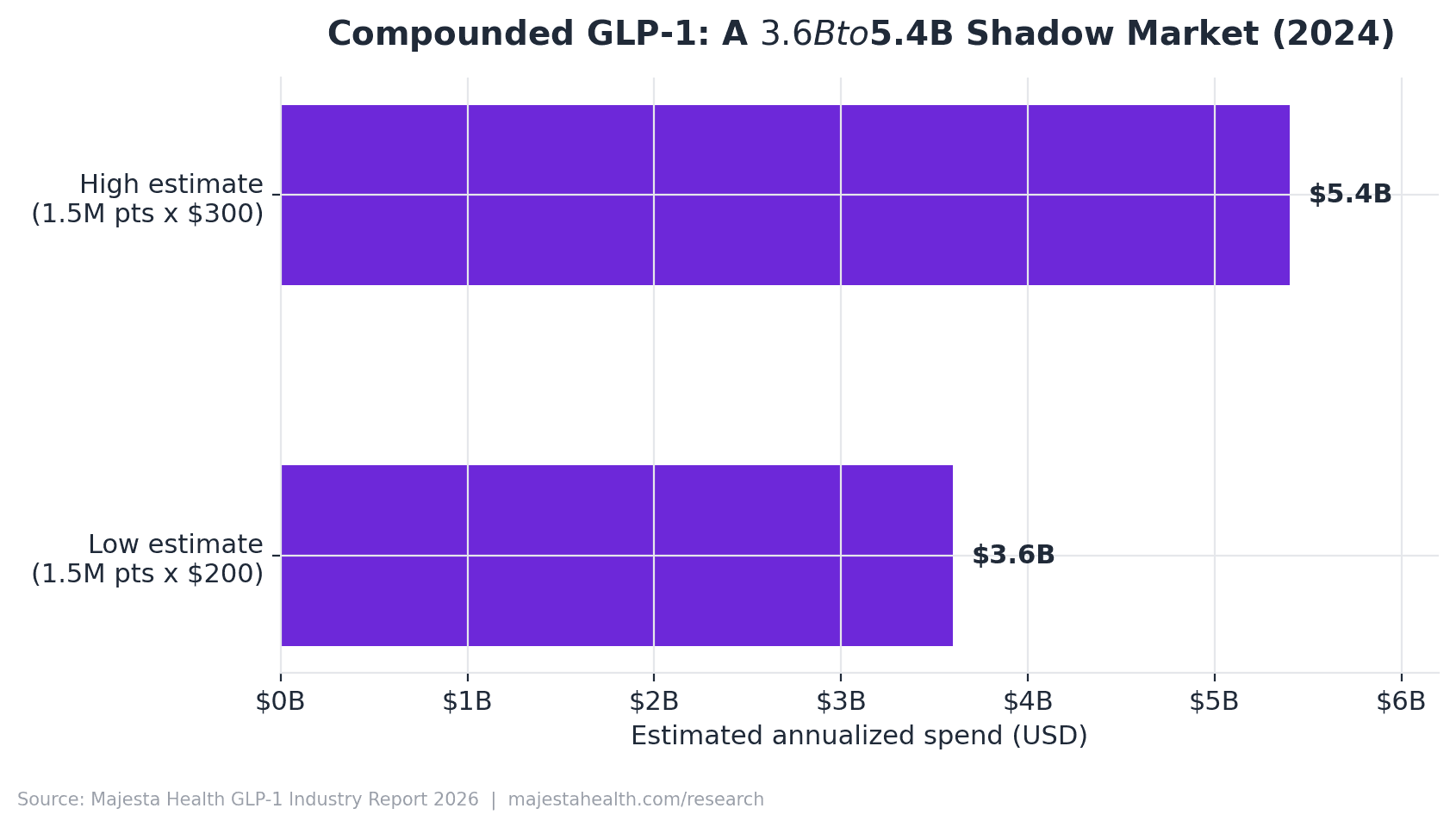

Sizing the compounded market

Unlike the brand market, the compounded GLP-1 market has no single quarterly disclosure. Using the National Pharmacy Compounding Coalition estimate of roughly 1.5 million patients on compounded GLP-1 in 2024 and a $200 to $300 blended monthly price gives an annualized compounded spend of roughly $3.6 billion to $5.4 billion in 2024. This is an order-of-magnitude estimate, not an audited number, and the compounded market in 2025 was approximately 5 to 10 percent of the size of the US brand-name market. Compounded medications are not FDA-approved as final products.

3Pricing landscape, brand versus compounded

The defining pricing story of 2026 is compression. For three years the market ran on a single arbitrage: compounded semaglutide and tirzepatide sold for roughly 85 percent less than brand list price, and that gap funded an entire telehealth distribution layer. In 2026 the gap is closing from both ends. Brand manufacturers launched cash-pay direct programs that cut effective brand prices in half, and the FDA shortage resolutions removed the legal basis for the cheapest "essentially a copy" compounding.

- The 2026 cash-pay price band for a monthly GLP-1 runs from roughly $99 to $449, by product type, dose tier, and prepay status.

- The historical compounded discount narrowed from roughly 85 percent to roughly 50 to 70 percent versus the comparable brand cash-pay option (a derived estimate).

| Provider | Monthly price (2026) | Product type | 2026 structural note |

|---|---|---|---|

| Hims & Hers | Brand Wegovy/Ozempic via Novo collaboration; limited compounded | Brand, limited compounded | Discontinued the $49 compounded semaglutide pill Feb 2026; announced Novo collaboration Mar 2026 |

| Ro | Zepbound vials $299 (2.5mg) to $449 (higher doses); Ro Body membership $39 first month then $74 to $149 | Brand (Lilly-aligned) | Repositioned around FDA-approved Zepbound vials |

| Medvi | ~$179 first month, ~$299 recurring range | Compounded | Among providers anchoring the post-exit compounded floor |

| Henry Meds | ~$197 to $297 injectable; oral ~$199 to $249 | Compounded | Plan-length pricing; 12-month prepay lowest |

| Mochi Health | $99 medication flat rate + $79 membership (~$178 all-in) | Compounded | Flat medication price regardless of dose |

| Calibrate | Program fee, medication separate | Coaching plus prescription | Behavior-program model, not a pure low-cost medication play |

| BeYou | Cash-pay tiers in the mid-hundreds | Compounded | Active in the consolidating compounded segment |

| Majesta Health | Express $179 first / $249 recurring; Essential $179 first / $299 recurring; Performance $329 first / $399 recurring | Compounded | Three-tier line; compounded products are not FDA-approved as final products |

Majesta appears as one provider among several, included for completeness, not as a recommendation. Advertised medication price and all-in monthly cost are different numbers, and the marketing-facing figure is almost always the lower one.

The price gap, by basis

| Comparison basis | Brand reference | Compounded reference | Implied discount |

|---|---|---|---|

| Semaglutide, brand list vs compounded | Wegovy list ~$1,000 to $1,350/mo | Compounded sema $99 to $299/mo | ~75 to 90% |

| Semaglutide, brand direct vs compounded | Wegovy direct ~$499/mo | Compounded sema $99 to $299/mo | ~40 to 80% |

| Tirzepatide, brand vials vs compounded | Zepbound vials $349 to $449/mo | Compounded tirz mid-hundreds | ~10 to 50% |

The plain reading: on semaglutide the compounded discount is still real but shrinking; on tirzepatide it has largely evaporated at the entry dose. When a patient can buy an FDA-approved Zepbound vial for $349, a compounded tirzepatide product priced near that figure competes on close to equal cost and needs a clinical or service rationale beyond price. Compounded medications are not FDA-approved as final products.

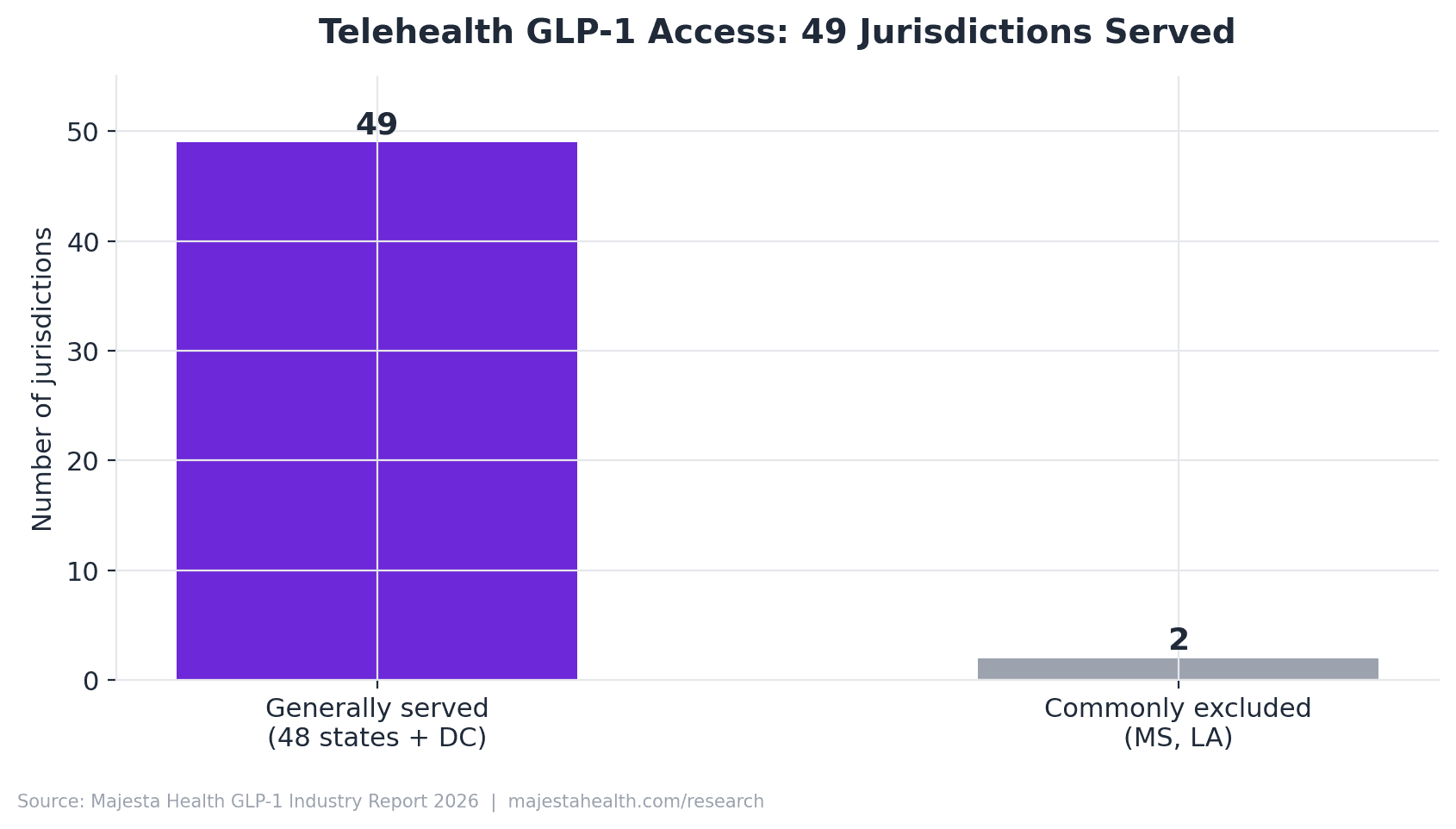

4The 50-state telehealth access scorecard

The defining access fact of the 2026 market is not federal. It is the patchwork of state medical-practice law that decides whether an online weight-management consultation can legally begin.

- 2 US states are commonly excluded by telehealth GLP-1 providers as of 2026: Mississippi and Louisiana, owing to stricter telemedicine and compounding shipment rules. The remaining 48 states plus the District of Columbia are generally served, though roughly a dozen impose first-visit conditions.

- GLP-1 receptor agonists are not federal controlled substances. Semaglutide and tirzepatide are not DEA-scheduled, so the Ryan Haight Act does not bar online prescribing. The binding constraint is state telehealth practice law.

The single most important access dimension is whether a state permits an asynchronous (store-and-forward) first visit or requires a synchronous (real-time audio-video) encounter to establish the provider-patient relationship. Asynchronous-permissive states support the fast online intake that defines the direct-to-consumer model.

| State | Establishment rule | Tier | Primary citation |

|---|---|---|---|

| Texas | Telemedicine relationship permitted by statute | Tier 1 / 2 (verify async) | Tex. Occ. Code 111.005 |

| California | Telehealth relationship and consent by statute | Tier 2 (consent disclosure) | Cal. Bus. & Prof. Code 2290.5 |

| Florida | Telehealth practice standards by statute | Tier 1 / 2 (verify async) | Fla. Stat. 456.47 |

| New York | Telehealth defined and authorized by statute | Tier 2 | NY Public Health Law 2999-cc |

| Ohio | Telehealth standards by administrative rule | Tier 2 | Ohio Admin. Code 4731-11-09 |

| Michigan | Telehealth authorized by statute | Tier 2 | Public Act 359 of 2016 |

| Illinois | Telehealth practice by statute | Tier 2 | 225 ILCS 60 |

| Mississippi | Stricter telemedicine establishment rules | Tier 3 (often excluded) | Verification pending |

| Louisiana | Stricter telemedicine and shipment rules | Tier 3 (often excluded) | Verification pending |

Because the prescribing clinician must hold an active license in each patient's home state, the rate-limiting resource is licensed-clinician coverage across states, not technology. A scorecard that is verified, dated, and re-checked each quarter is a compliance asset, not a one-time deliverable. Compounded medications are not FDA-approved as final products.

5Supply chain and shortages, 2022 to 2026

- Semaglutide injection products were on the FDA Drug Shortage List for approximately 1,058 days (March 2022 to February 21, 2025), about 2.9 years.

- Tirzepatide injection products were on the list for approximately 660 days (December 2022 to October 2, 2024, with a brief late-2024 reconsideration), about 1.8 years.

- These shortages were the legal precondition for the entire "essentially a copy" compounded GLP-1 market that emerged in 2022 to 2024.

The shortages were primarily demand-driven, not supply-disrupted. The 2021 publication of STEP 1 triggered a prescribing wave that Novo Nordisk's manufacturing footprint had not been built to serve, and the same dynamic followed SURMOUNT-1 in 2022. Adding fill-and-finish capacity for injectable products typically takes 24 to 36 months, and a pen-device assembly bottleneck persisted even after active-ingredient supply caught up.

| Molecule | FDA resolution | 503A cease-compounding deadline | 503B deadline |

|---|---|---|---|

| Tirzepatide | December 19, 2024 | February 18, 2025 | March 19, 2025 |

| Semaglutide | February 21, 2025 | April 22, 2025 | May 22, 2025 |

Under section 503A of the Federal Food, Drug, and Cosmetic Act, state-licensed pharmacies may prepare drugs "essentially a copy" of an FDA-approved product only while that product is on the shortage list. When the FDA declared both shortages resolved, the legal basis for that copy market closed. What survived was the clinically distinct segment: sublingual troches, B12 and carnitine combinations, custom dosing, and documented clinical-need cases. The vanilla "buy compounded semaglutide because it is cheaper" model is no longer a lawful basis for new prescriptions. Compounded medications are not FDA-approved as final products.

6Patient demographics and reported outcomes

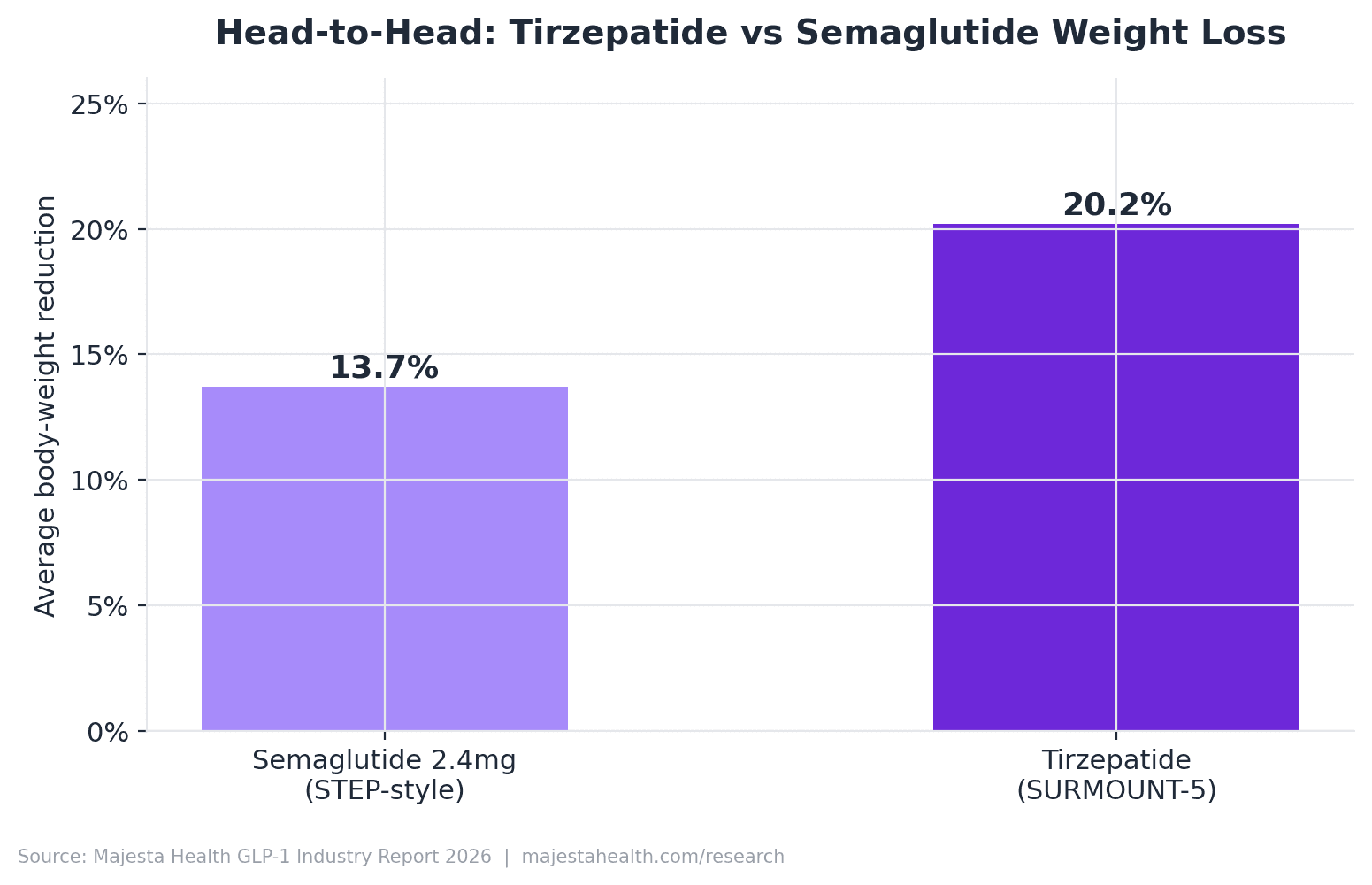

Across the major randomized controlled trials, mean body weight reduction at the primary endpoint ranged from roughly 15 percent to 21 percent for the two leading molecules.

Critical framing: every percentage here is a published trial result measured in a controlled study population. These figures are not Majesta Health promises, and they are not what any individual patient will achieve. Individual results vary. The trials studied brand-name molecules, not compounded formulations. Compounded medications are not FDA-approved as final products.

| Trial | Molecule / dose | Mean % reduction | Timepoint | Citation |

|---|---|---|---|---|

| STEP 1 | Semaglutide 2.4 mg | 14.9% | Week 68 | Wilding 2021 |

| STEP 4 | Semaglutide 2.4 mg | ~17.4% (continued arm) | Week 68 | Rubino 2021 |

| STEP 8 | Semaglutide 2.4 mg | ~15.8% | Week 68 | Rubino 2022 |

| SURMOUNT-1 | Tirzepatide (up to 15 mg) | up to 20.9% | Week 72 | Jastreboff 2022 |

| SURMOUNT-2 | Tirzepatide | ~14 to 15% | Week 72 | Garvey 2023 |

| SELECT | Semaglutide 2.4 mg | 20% relative MACE reduction | Up to ~40 months | Lincoff 2023 |

SELECT is the trial most often misquoted. Its headline result was not a weight figure. It reported a 20 percent relative reduction in major adverse cardiovascular events in non-diabetic patients with obesity and established cardiovascular disease, and it should be cited as a cardiovascular endpoint, not blended into the weight numbers.

Trial versus real-world outcomes

Trial cohorts were screened, force-titrated to target dose on a protocol schedule, supported for adherence, and paired with structured lifestyle counseling. Real-world patients differ on every dimension. Published real-world analyses commonly place one-year discontinuation in roughly the 30 to 50 percent range, depending on dataset and definition. The withdrawal-design trials (STEP 4, SURMOUNT-4) both showed weight regain after stopping: the medication's effect is maintained while it is taken and is not a one-time, permanent intervention.

The real-world telehealth weight-management cohort skews female (frequently cited around two-thirds), clusters in the 30 to 55 age band, and is largely cash-pay. These are survey-based estimates, not a national registry, and reflect who can currently afford and access cash-pay telehealth rather than who medically qualifies.

7Compounded GLP-1 market analysis, 2026

Disclosure. Compounded medications are not FDA-approved as final products. The compounded GLP-1 preparations discussed here are prepared by state-licensed pharmacies under physician prescription and are not reviewed by the FDA for safety, efficacy, or quality as finished products.

- Estimated patients on compounded GLP-1, 2024: roughly 1.5 million Americans (industry estimate, not audited).

- Estimated compounded GLP-1 spend, 2024: roughly $3.6 billion to $5.4 billion annualized (order-of-magnitude only).

- Compounded share of the US brand-name market, 2025: roughly 5 to 10 percent.

The most important fact about the compounded market in 2026 is that it is a different market than it was in 2024. Between 2022 and early 2025 it was overwhelmingly a shortage-driven copy market competing on price. The 2025 resolutions closed that window. What did not close was the long-standing exemption for clinically distinct compounded formulations, which does not depend on a shortage. The result is a market that shrank in volume but shifted in character: smaller, more clinically justified, more documentation-intensive, and harder to enter.

| Dimension | 503A pharmacy | 503B outsourcing facility |

|---|---|---|

| Prepared for | A specific patient on a valid prescription | Bulk, may be prepared without a patient-specific prescription |

| Registration | State board of pharmacy licensed | Registered with and inspected by the FDA |

| Manufacturing standard | State pharmacy practice standards | Federal current Good Manufacturing Practice (cGMP) |

| FDA inspection | Not routinely FDA-inspected | Routinely FDA-inspected |

Neither pathway produces an FDA-approved finished product. Three verifiable signals separate a legitimate compounder from a gray-market seller: active state board of pharmacy licensure, NABP accreditation, and LegitScript Healthcare Merchant Certification. A gray-market seller that takes cash for unbranded vials and cannot be matched to a state board license holds none of these. Compounded medications are not FDA-approved as final products.

As one worked example of the legitimate-compounder structure, a pharmacy such as Belmar Pharma Solutions holds LegitScript certification and NABP accreditation, operates under both 503A and 503B status, and a telehealth provider partnering with that profile illustrates the full credentialing chain. This is one example of the structure, not a recommendation or a conclusion about the market, and the products such a model produces remain not FDA-approved as final products.

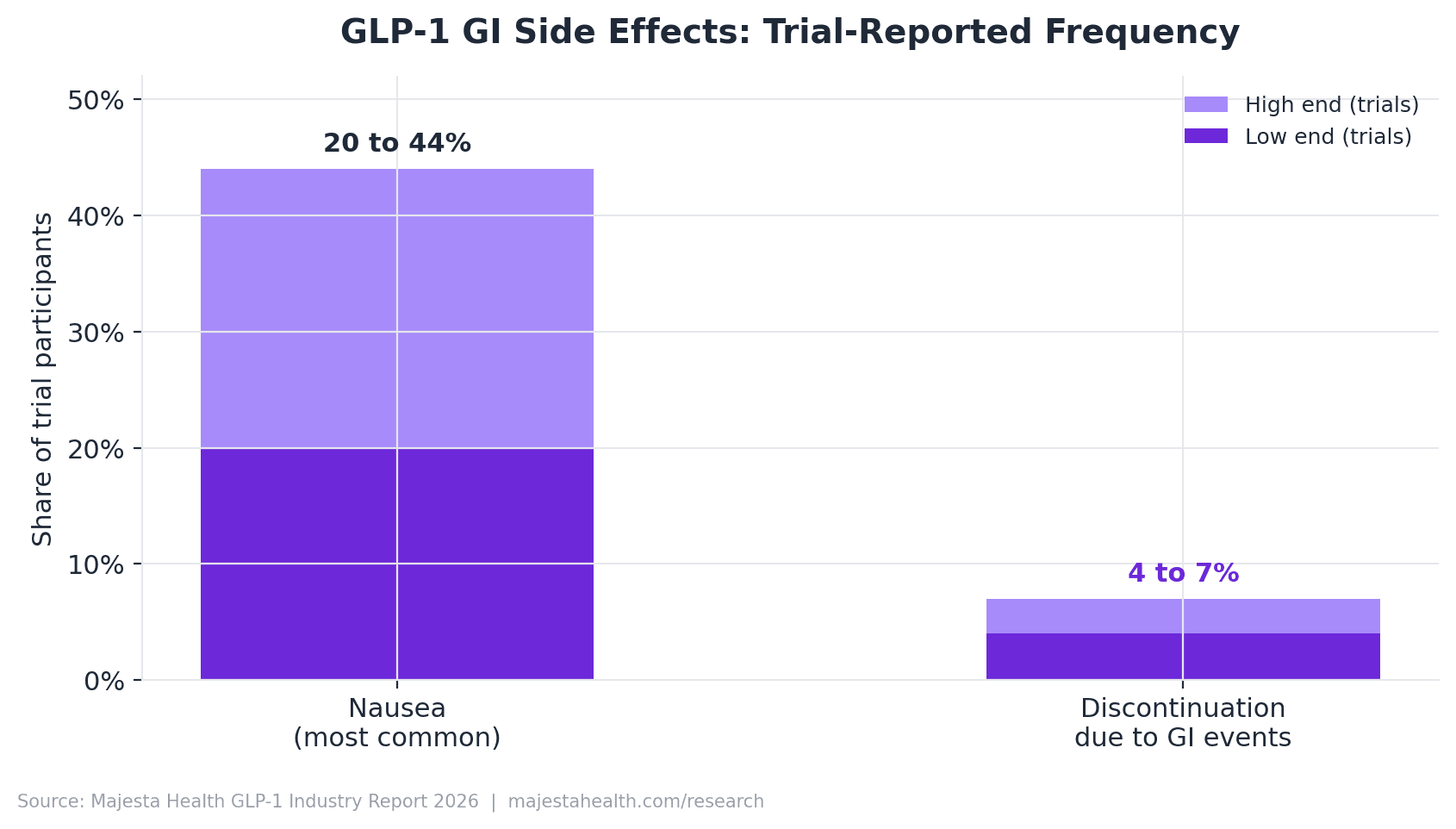

8Side effect reporting analysis

The GLP-1 class has a well-characterized safety profile. Gastrointestinal events are the most common adverse events, they are usually mild to moderate, and they tend to peak during dose escalation and ease over time.

- Nausea, the single most-reported event, appears in roughly 20 to 44 percent of trial participants, varying by molecule, dose, and titration schedule.

- Discontinuation due to GI side effects in trials is commonly roughly 4 to 7 percent.

| Frequency tier | Adverse events |

|---|---|

| Very common (GI) | Nausea, vomiting, diarrhea, constipation, abdominal pain |

| Common | Decreased appetite, dyspepsia, eructation, fatigue, injection-site reactions, headache |

| Less common | Gallbladder disease, dehydration secondary to vomiting or diarrhea, acute kidney injury secondary to dehydration |

| Rare but serious | Pancreatitis, ileus, severe hypersensitivity, pulmonary aspiration under anesthesia |

| Boxed warning | Thyroid C-cell tumors (rodent studies); contraindicated with personal or family history of medullary thyroid carcinoma or MEN 2 |

How to read FAERS data. The FDA Adverse Event Reporting System is a passive, voluntary database. A report does not establish that the drug caused the event, there is no denominator so raw counts cannot become rates, reporting is biased by media and litigation, and duplicates exist. This report uses FAERS only for signal detection, never to compute a frequency. Every percentage in this chapter comes from FDA labeling or pivotal trial publications, not from FAERS counts.

A genuine recent development: in 2023 and 2024 the FDA updated GLP-1 labeling to reflect reports of pulmonary aspiration during anesthesia and deep sedation, attributed to delayed gastric emptying. Anyone scheduled for surgery, an endoscopy, or any procedure requiring sedation should tell both their prescriber and the procedural team that they take a GLP-1 medication, well in advance. Compounded semaglutide and tirzepatide contain the same active molecules and carry the same molecule-level profile; formulation variants can change the tolerability experience, and compounded medications are not fda-approved as final products.

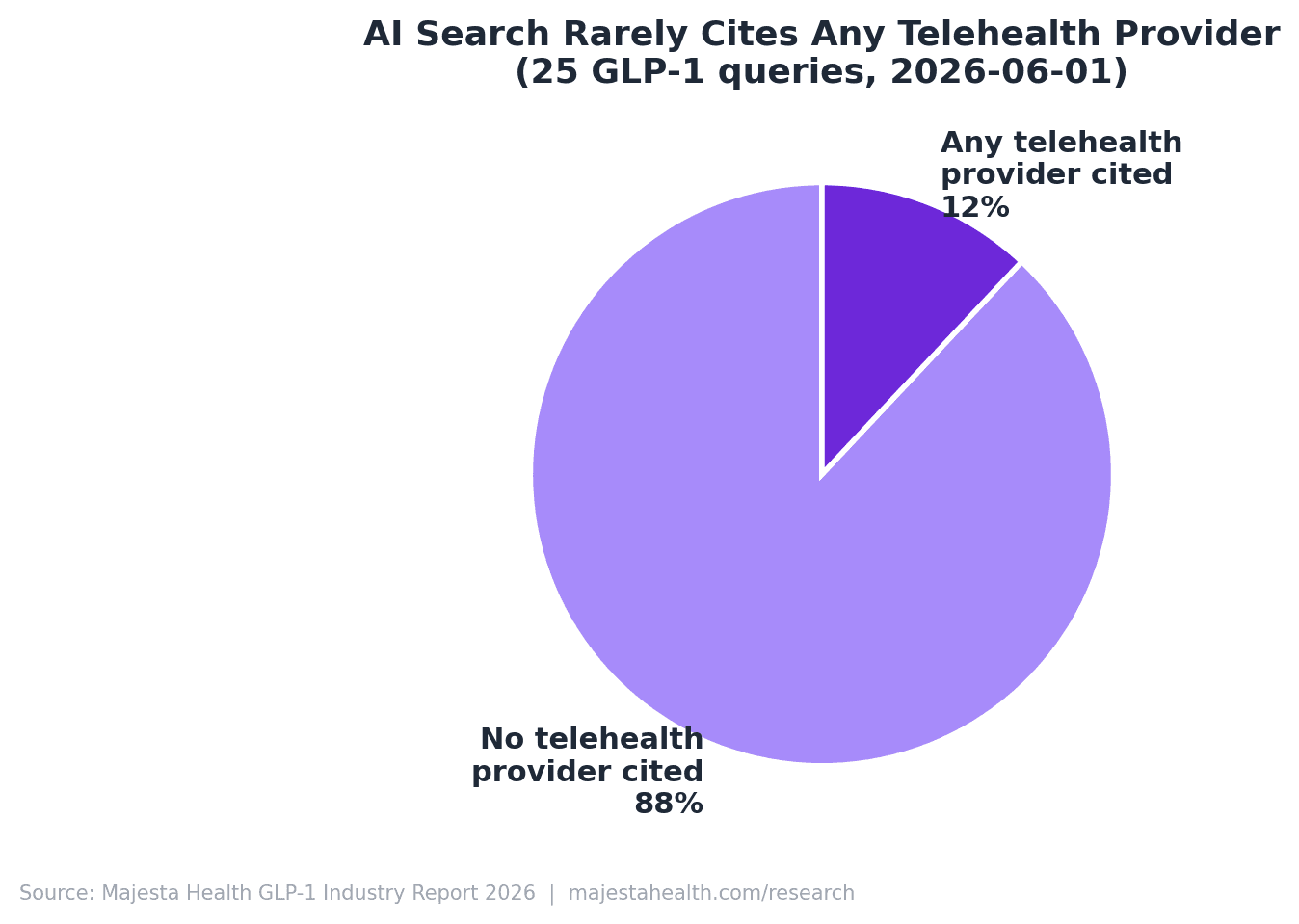

9AI search visibility analysis

This chapter reports original measurement. Majesta Health runs a weekly monitor that asks a fixed panel of 25 consumer GLP-1 queries against two AI engines (OpenAI gpt-4o-mini and Gemini 2.0 Flash with search grounding) and counts which domains are cited. The finding is counterintuitive: as of mid-2026, AI search for GLP-1 weight management almost never cites a telehealth provider.

Two disclosures up front. Majesta is the publisher and is in the tracked set, and at the time of this data it was cited on 0 of 25 queries across both engines. We are not above the data we report. Where a competitor domain appears, we report it as a data point, not an endorsement or a criticism.

| Domain | Citations | Rate |

|---|---|---|

| ro.co | 3 | 12.0% |

| hims.com | 2 | 8.0% |

| majestahealth.com (publisher) | 0 | 0.0% |

| medvi.org | 0 | 0.0% |

| henrymeds.com | 0 | 0.0% |

| joincalibrate.com | 0 | 0.0% |

| mochihealth.com | 0 | 0.0% |

The 12 percent is not evenly distributed. Telehealth citations cluster on a narrow band of high commercial-intent queries ("best telehealth providers for GLP-1," "compare Hims, Ro, Medvi"). Pure clinical, safety, and educational queries ("is compounded semaglutide safe," "tirzepatide vs semaglutide," "what is sublingual semaglutide") returned zero telehealth providers with near-perfect consistency across three weekly snapshots.

Three read-throughs follow. With 88 percent of GLP-1 queries returning no telehealth provider, the AI-answer channel is barely contested. The only two providers that appear, Ro and Hims, are the two largest direct-to-consumer brands, which suggests current AI citation is downstream of brand mention volume, not content depth. The clinical-and- safety query set, where no provider is cited, is the open opportunity. Majesta held at 0 of 25 across all three weeks, consistent with a recently launched domain.

10Telehealth platform comparison

Disclosure. Where this chapter describes providers selling compounded GLP-1 preparations, those products are compounded medications and are not FDA-approved as final products. The chapter cites only public pricing and public marketing and attributes no motive to any company.

The single most important structural fact about the 2026 platform set is that it is no longer one category. The shortage resolutions split the field into three business models that now compete for the same patient with different products.

- Brand-pivot platforms moved their weight programs onto FDA-approved products. Hims & Hers discontinued its $49 compounded semaglutide offering in February 2026 and announced a Novo collaboration in March 2026; Ro anchored on FDA-approved Zepbound vials.

- Compounded specialists (Medvi, Henry Meds, Mochi, BeYou, Majesta) continued selling compounded preparations under the clinical-need pathway, differentiating on formulation and service rather than a single low price.

- Calibrate is a third type: a coaching program layered on prescription access, where the coaching, not the medication price, is the product.

Majesta is the publisher of this report and appears as one example among several, not as the recommended conclusion. A patient comparing GLP-1 telehealth providers in 2026 is often comparing businesses that no longer sell the same kind of thing.

A neutral evaluation framework

This framework applies equally to every platform, Majesta included, and points to no recommended answer. Check four things. Licensing: confirm the prescriber is licensed in the patient's own state and that a real medical evaluation occurs. Pharmacy type: ask whether the pharmacy is a state-licensed 503A pharmacy or an FDA-registered 503B facility, and whether it holds NABP accreditation and LegitScript certification. Physician oversight: determine whether a licensed clinician reviews the intake and is reachable for dose questions. Transparency: read past the headline price to the all-in monthly cost, commitment length, and cancellation terms. Compounded medications are not FDA-approved as final products.

11Future outlook, 2026 to 2030

Every forward view is wrong in specifics. This chapter separates what is locked (approved products, disclosed pipelines, statutory patent terms), what is conditional (trial readouts, regulatory determinations, payer decisions), and what is speculative (market sizes that depend on all of the above). None of it is investment advice.

The 2022 to 2025 boom ran on two molecules. The 2026 to 2030 period introduces a wider field of investigational programs: CagriSema (Novo Nordisk), retatrutide (a triple agonist from Eli Lilly), orforglipron (an oral small-molecule GLP-1 from Eli Lilly), higher-dose oral semaglutide, and survodutide (Boehringer Ingelheim and Zealand Pharma). Each is investigational for obesity and not FDA-approved unless and until the FDA acts. An oral that manufactures like a conventional small molecule, if approved, changes the supply math behind the 2022 to 2024 shortages, since tablet capacity is not constrained like injectable pen fill-and-finish.

Semaglutide's core US composition-of-matter protection is generally described as running into the early 2030s (commonly cited around 2031 to 2032, subject to litigation and settlements), with tirzepatide later, into the mid-2030s. The steepest brand price declines are therefore a post-2030 story. Coverage is the largest swing factor and is unsettled: Medicare statute has historically barred Part D from covering weight-loss drugs, with coverage existing only for approved comorbid indications, while employer and commercial plans expand slowly behind prior authorization and BMI gating.

| Scenario | Core assumption | Illustrative 2030 US brand market |

|---|---|---|

| A. Broad expansion | Multiple approvals, conditional coverage gains | ~$90 to $120 billion |

| B. Steady state | Managed demand, persistent payer friction | ~$70 to $90 billion |

| C. Pressured | A safety, policy, or pricing shock | ~$55 to $70 billion |

The center of gravity sits between A and B: the category almost certainly remains larger in 2030 than in 2025, and the largest variable is not science but who pays. Compounded medications are not FDA-approved as final products.

12Methodology limitations

Usefulness depends on honesty about boundaries. This is the deliberate accounting of what the report did not measure.

- Pricing reflects advertised rates, not verified transactions. No transaction receipt was audited; advertised medication price and all-in monthly cost are different numbers.

- Outcomes are trial-population figures. The 15 percent to 21 percent range is a population mean under favorable study conditions, not an individual expectation, and the trials studied brand-name molecules, not compounded formulations.

- FAERS cannot establish causation. Any frequency figure in the report comes from FDA labeling or pivotal trials, never from FAERS counts.

- The AI citation panel is a 25-query snapshot, not an exhaustive census, bounded by the query set, the two engines, and the weekly timing.

- The state scorecard is a point-in-time reading of changing law and is a research synthesis, not legal advice.

- The publisher is a market participant, disclosed openly. Majesta Health sells telehealth GLP-1 services. That is a conflict of interest, stated plainly. Chapter 9 is the clearest test: it discloses the 0 of 25 finding that reflects poorly on the publisher and publishes it anyway.

Compounded medications are not FDA-approved as final products.

13Glossary

- GLP-1 receptor agonist

- A medication that activates the GLP-1 receptor, producing effects similar to the natural gut hormone: lower blood sugar, slower gastric emptying, and reduced hunger.

- Dual agonist

- A medication that activates two receptors at once. Tirzepatide is a dual GIP and GLP-1 receptor agonist, the basis for its higher measured weight reduction in trials.

- Compounded medication

- A drug prepared by a licensed pharmacy for a specific patient (or, for outsourcing facilities, in batches) rather than manufactured under FDA approval. Compounded medications are not FDA-approved as final products.

- 503A pharmacy

- A state-licensed pharmacy that prepares compounded preparations for a specific patient on a valid prescription. Not routinely FDA-inspected; its output is a compounded preparation, not an FDA-approved drug.

- 503B outsourcing facility

- A compounding facility registered with and inspected by the FDA that may prepare larger batches under federal cGMP. A higher manufacturing-oversight bar than a 503A pharmacy, but its output is still a compounded preparation, not an FDA-approved drug.

- FAERS

- The FDA Adverse Event Reporting System, a passive, voluntary database. A report does not establish causation, and raw counts cannot be converted into rates because the database has no patient denominator.

- Async vs synchronous telehealth

- Asynchronous (store-and-forward) telehealth uses an intake questionnaire reviewed by a clinician with no live visit. Synchronous telehealth requires a real-time audio-video encounter. Which one a state permits for a first visit is the key access variable.

- Titration

- The gradual, scheduled increase of a dose from a low starting point to a target maintenance dose, used to reduce gastrointestinal side effects that peak during escalation.

14Citations and sources

Every headline statistic traces to a named source a reader can independently check: a regulatory database, a company financial disclosure, a peer-reviewed clinical trial, a public pricing page, or a named directory. Where a figure is an industry estimate, the report labels it as such at the point of use. The published edition attaches specific URLs and accessed-on dates; we deliberately did not fabricate specific links.

- FDA Drug Shortage Database. Government regulatory database. Chapters 2, 5, 7.

- FDA Adverse Event Reporting System (FAERS). Government surveillance database. Chapter 8.

- FDA prescribing information and product labeling, semaglutide and tirzepatide. Chapters 8, 13.

- State medical-practice and pharmacy statutes (cited in Chapter 4). Primary state law.

- Novo Nordisk investor relations and 2025 annual report. Chapter 2.

- Eli Lilly investor relations and 2025 annual report. Chapter 2.

- STEP 1 (Wilding et al., NEJM 2021). Chapter 6: semaglutide 14.9 percent at week 68.

- STEP 4 (Rubino et al., 2021) and STEP 8 (Rubino et al., 2022). Chapter 6.

- SURMOUNT-1 (Jastreboff et al., NEJM 2022). Chapter 6: tirzepatide up to 20.9 percent at week 72.

- SURMOUNT-2, 3, 4 (Garvey 2023, Wadden 2023, Aronne 2024). Chapter 6.

- SELECT (Lincoff et al., NEJM 2023). Chapter 6: 20 percent relative MACE reduction.

- SUSTAIN trial program (semaglutide in type 2 diabetes). Reference.

- Telehealth provider public pricing pages (Hims and Hers, Ro, Medvi, Henry Meds, Mochi Health, Calibrate, BeYou, Majesta Health). Chapters 3, 9, 10.

- Novo Nordisk and Eli Lilly cash-pay direct program announcements. Chapter 3.

- SEMrush search-analytics platform. Keyword-volume snapshot.

- NABP (National Association of Boards of Pharmacy) directory. Chapter 7.

- LegitScript Healthcare Merchant Certification directory. Chapters 2, 7.

- National Pharmacy Compounding Coalition industry estimate. Chapters 2, 7 (labeled an estimate).

- Majesta Health AI citation monitor (25-query GEO panel). Chapter 9: original dataset.